Property Owners Insurance Coverage Skyrocketed In These States Risk insurance policy may leave out particular types of damages, such as losses from a flooding or a sinkhole. For residential or commercial properties susceptible to these threats, purchasing optional added home owners insurance protection might be advisable. That's leading some people to downsize coverage or even do without. As natural disasters continue to impact communities worldwide, it's natural to have inquiries concerning exactly how they can impact your insurance policy protection. Luckily, the majority of home owners' insurance policies will certainly cover any wind damage and even wind-driven rainfall as a result of a storm. However, home insurance coverage doesn't supply insurance coverage for flooding damages during a typhoon storm surge. Purchasing flooding insurance coverage is usually an excellent concept to give you an added layer of defense. Open-peril policies will cover every one of the damages unless it's a specifically omitted hazard. There have been 357 disasters costing more than $1 billion each in the U.S. because 1980. The chart below programs the four most common disasters in the Learn more U.S., which additionally include losses from cyclones and hurricanes. Power outages, without various other physical damage to the framework of your home, aren't covered as part of conventional homeowners insurance policies.

Which Natural Disasters Does My House Owner's Insurance Policy Cover?

As an example, an HO-3 consists of open-peril home insurance coverage, but it does have a few significant exclusions, which include quake, flooding, and disregard. On the various other hand, named-peril plans will just cover the particular threats noted within the policy, as it doesn't use as broad protection contrasted to open-peril plans. In some cases homeowner's insurance can include both open-peril and named-peril sections, as it is very important to reach out to your insurance agent to learn about these information. As a whole, coverage for wildfire damage is normally included in homeowners' and commercial property insurance plan. These plans generally cover damages triggered by wildfires to frameworks like homes and structures as well as individual belongings.There are some good reasons to check your homeowners insurance heading into spring - CNBC

There are some good reasons to check your homeowners insurance heading into spring.

Posted: Fri, 13 Mar 2020 07:00:00 GMT [source]

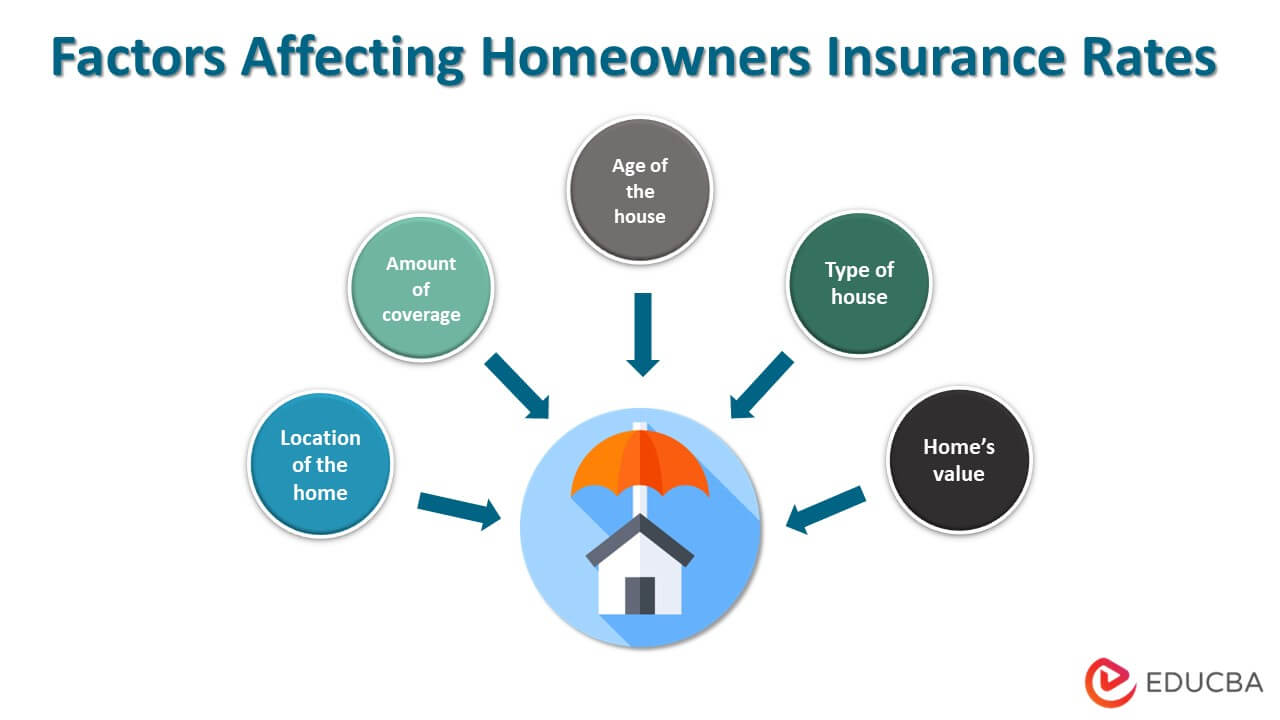

Why House Owners Insurance Rates Are Increasing

Picking a greater deductible will normally decrease your home insurance costs yet you will get much less money if you submit a damage or theft claim. However if a tree falls due to a trouble covered by your policy and blocks your driveway, your policy might cover debris elimination approximately a defined limitation. For instance, a plan may pay up to $1,000 for debris elimination expenses. It is essential to keep in mind that even if you haven't directly experienced an all-natural catastrophe, your insurance policy rates can still be impacted. This is since insurance provider consider wider geographic and ecological elements when figuring out rates. All-natural calamities occasionally trigger explosions, whether of a gas line, high-voltage line, electric post, or another thing that might be influenced by the all-natural disaster. These kind of explosions are covered by a lot of home insurance plan. It is important to remember that explosions because of war, intentional acts, or nuclear hazards, would certainly not usually be covered.- Lemonade might cover damages triggered by a fire adhering to an earthquake, which is an usual consequence of a quake.Without obligation home insurance, a proprietor might be directly responsible for covering lawful expenses and losses sufferers sustain after injury.The graph listed below highlights the typical cost of home insurance policy in numerous states susceptible to all-natural catastrophes, along with the typical cost of home insurance policy in high-risk cities within those states.Plans do vary, however, so for your own comfort, check your own for the particular risks covered.